Financial management ensures the efficient and effective management of money (funding) to accomplish the objectives of the organisation.

Previous

Chapter 28: Resource managementThe Teal Book: Part E

Financial management ensures the efficient and effective management of money (funding) to accomplish the objectives of the organisation.

All project delivery has a cost. This can be direct, through funding provided for the purpose, or indirect, through the use of organisational resources. Financial management is how a portfolio, programme or project understand their costs, secure funding and control spending through delivery and into operations.

In government, project delivery involves using public resources. Financial management provides the information to show that public funding has been used in line with the terms agreed by Parliament, and that the accounting officer standards of regularity, propriety, value for money and feasibility, as set out in Managing public money, are upheld. This is typically the case, even for work that is funded through private finance, where public funding is normally used for overseeing, planning and delivery, and there might be commitments for future expenditure.

Effective financial management also makes sure that the rules on using public money are factored into planning and managing budgets, and that the necessary accounting standards are met.

Financial management in project delivery covers managing:

It can also involve other financial processes such as grant administration, debt recovery, tax, asset management and investment appraisal, and management of financial risk, including the prevention of fraud, bribery and corruption.

All financial management in government, including for project delivery, should follow HM Treasury’s Managing public money (requires sign in) and its supplementary guidance for accounting officers. It should also follow the standards in the Government Functional Standard for Finance, Government Functional Standard for Internal Audit, Government Functional Standard for Counter Fraud, Government Functional Standard for Debt and Government Functional Standard for Grants.

Everyone working in government project delivery has a responsibility to ensure that public resources are managed and used efficiently, effectively and in line with the principles and standards in Managing public money (requires sign in) and government functional standards.

Most project delivery work requires the involvement of qualified finance professionals, working within the immediate team, the sponsoring organisation and other organisations, particularly HM Treasury. Accountability and responsibility for financial management should be clearly defined within the governance and management framework and reviewed regularly.

Financial management in government project delivery takes place within a formal framework of accountabilities governing the use of public money, set out in Managing public money.

The government has the responsibility to control and account for public expenditure. Ministers seek to implement government policies and deliver public services through their organisations, but only when Parliament has granted the right to raise, commit and spend resources.

HM Treasury is responsible to Parliament for the control of public resources. It allocates funding approved by Parliament to government departments and, through them, to their arm’s length bodies. HM Treasury ensures that government organisations have adequate legal authority to spend the public resources voted to them by Parliament through formal approval of legislation and policy decisions with public expenditure implications. Where spending proposals exceed an organisation’s delegated authority limit, or are novel, contentious or repercussive, HM Treasury scrutinises and approves business cases through the Treasury approval process for projects and programmes (requires sign in).

In individual government organisations, overall accountability for financial management sits with the organisation’s accounting officer, usually supported by a chief finance officer or finance director. The accounting officer is accountable to Parliament for ensuring that the organisation’s actions meet the accounting officer standards of regularity, propriety, value for money and feasibility. They are also responsible for managing the governance and management framework for financial management within the organisation.

Funding for arm’s length bodies is usually delegated as grant-in-aid by the sponsoring government department. The accounting officer in the arm’s length body is usually accountable to the principal accounting officer in the sponsoring department for use of allocated funding as well as to Parliament. For more information on this and other forms of grant, see the Government Functional Standard for Grants.

The accounting officer is accountable for approving all significant initiatives, policies, programmes and projects in advance, taking account of any internal delegated authorities. This is usually managed through an investment scrutiny and approval process overseen by the organisation’s investment committee and chaired by the accounting officer or chief finance officer on their behalf.

Government Major Projects Portfolio and accounting officer assessments

For programmes and projects in the Government Major Projects Portfolio, an accounting officer assessment must be produced at decision points. A summary of the assessment should be published. (see Accounting officer assessments: guidance for more information).

The portfolio director, in a portfolio, or senior responsible owner in a programme or project, is accountable for effective financial management. This includes owning the financial management framework and plan, and leading work to identify and secure funding. For a portfolio, this is often part of the organisation’s spending review funding bid. For a programme or project, this is usually through annual business planning or the organisation’s investment scrutiny and approval process.

The portfolio, programme or project manager, is accountable for developing and implementing the financial management framework and finance plan, and for ongoing financial control, reporting and accounting.

Some financial management activities may be delegated to a work package manager. Financial management work is normally led by a finance manager and supported by a finance team, usually based in a support office.

More detail on professional finance roles is set out in the Government Finance Function’s Career framework.

Financial management in project delivery needs to integrate with the wider financial management and accounting arrangements in the sponsoring organisation.

At portfolio level, a portfolio can cover the whole of an organisation’s capital investment and resource spend. Programme and project financial arrangements also need to be integrated with the sponsoring organisation. Even where a separate organisation (usually an arm’s length body) is created to deliver work, its accounts are normally consolidated into the sponsoring organisation’s accounts.

Financial management arrangements should be consistent with the sponsoring organisation’s processes and use their financial management and accounting systems wherever possible. Accounting data should be captured consistently across portfolios, programmes and projects so that costs, income, savings and forecasts can be compared and reported at each level.

Funding availability cannot be assumed, even where there is strong support for the work and a compelling business case, as organisations have to balance many different priorities in pursuit of their objectives. A realistic funding plan and a commitment from the funder are needed before a business case is approved. Approval then either triggers the release of funding for part or all of the work, or provides authority for expenditure where funding is already held in organisation budgets.

Funding is allocated by financial year. Allocations cannot be moved from one financial year to the next without agreement from HM Treasury and updating the business case. Funding sources can include those from grants, estimates, tax, public dividend capital, public borrowing, external borrowing and income generation, as set out in Managing public money.

There are also strict rules on expenditure classifications agreed with HM Treasury, including distinctions between administrative and programme spend, and between resource and capital spend. These are described in the Consolidated budgeting guidance.

Some government funding is also delegated on a ring-fenced basis by UK Parliament or HM Treasury for specific purposes, for example Official Development Assistance (see 10.8 on tailoring to international work).

Some project delivery work involves the use of private finance, for example joint ventures with private sector partners. Where this is being considered, advice should be sought from the National Infrastructure and Service Transformation Authority. These arrangements require HM Treasury approval.

Business case approval and spending authorisation are not the same thing, but in practice are often linked:

Both form part of the government control framework for programmes and projects, as set out in Managing public money. Business case approval also depends on other requirements being met. For example, functional controls are set out in the Department’s Memorandum of Understanding with HM Treasury.

Approval and authorisation can be for the next phase of the work or for all of it, depending on the business case and other considerations, for example for risk and future funding availability beyond the current spending cycle.

Business case approvals and spending authorities are governed by a department’s delegated authority limit (DAL). Spending proposals are required to follow the Treasury approvals process for projects and programmes (requires sign in) if they:

This process provides different levels of scrutiny depending on the scale and complexity of the programme or project concerned.

Government and Departmental Major Projects and HM Treasury approvals

Programmes and projects in the Government or Departmental Major Projects Portfolio require HM Treasury approvals preceding decision points. See the Treasury approval process for projects and programmes (requires sign in) for more information.

Business cases that do not require HM Treasury’s approval may be approved within the sponsoring department using the departmental investment approvals process, in line with their delegated spending authority arrangements. Similar delegated arrangements are in place between departments and their arm’s length bodies.

Authority for spending within the delegated authority limit is held by the accounting officer, and delegated further as appropriate. Senior responsible owners should have delegated spending authority within agreed limits and are encouraged to delegate day-to-day spending authority to programme or project managers, who can delegate further if appropriate.

Delegated authority for spending can be provided to develop proposals and prepare a business case before formal approval, in line with the limits on modest or temporary expenditure set out in Managing public money. Once an investment case has been approved, the senior responsible owner or their delegate has authority for expenditure, subject to the terms of the delegation. Spending authority and other delegated authorities, for example on procurement, should be set out in a delegation letter to the senior responsible owner and in individual letters to anyone that authority is further delegated to.

Financial planning and forecasting involves dealing with uncertainty.

First, make uncertainty visible. Financial analysis and modelling should be robust and evidence-based, but where uncertainty exists, it should be stated clearly, with a range of plausible outcomes presented. Specialist advice should be sought on methodology where needed.

Second, build contingency into the plan and business case. The financial case should include contingency to cover financial risks and liabilities. The economic case should account for uncertainty and risk in its modelling. As the work progresses and projections become more certain, assumptions should be adjusted and contingency updated.

Third, hold contingency centrally. Contingency should be held within the sponsoring organisation, not allocated as part of the budget for the work. This is because government is effectively self-insured: residual contingency in the financial case is converted into nominal prices and used to estimate the contribution to the organisation’s reserves. Arrangements for managing contingency, drawing it down and accounting for its use should be included in the governance and management framework.

Financial analysis and modelling should conform to the Government Functional Standard for Analysis, supported by the Aqua book (requires sign in). The Green book (requires sign in) provides specific guidance on handling uncertainty, optimism bias and risk in business cases.

In portfolios, funding is allocated in line with agreed priorities. Spend against budget should be reported and analysed regularly to identify actual and forecast underspends and overspends. Where variances occur, the portfolio director should flag these promptly and take decisions on addressing them.

In programmes and projects, the senior responsible owner is accountable for financial discipline.

Accurate planning, recording and reporting of spend matters because:

Everyone working in government has a responsibility to protect public money. Accounting officers are responsible for managing fraud, bribery and corruption risks as part of their accountability to Parliament.

Senior responsible owners should balance preventative and detective controls to tackle and deter fraud, bribery, corruption and other malpractices. For all proposals, proportionate counter fraud measures should be built into the design as a constraint and therefore as a requirement of all viable options.

Government major projects and initial fraud assessments

New programmes or projects joining the Government Major Projects Portfolio (GMPP) are required to complete an initial fraud impact assessment in line with Professional standards and guidance for fraud risk assessment in government. Assessments should be submitted to the Public Sector Fraud Authority for assurance before spending approval.

This assessment:

The senior responsible owner should complete this with support from local counter fraud teams.

Once spending is approved, a full fraud risk assessment should be completed in line with the Professional standards and guidance for fraud risk assessment in government and monitored through the life cycle.

For further information see the Government Functional Standard for Counter Fraud.

The financial management framework should reflect the mandate and objectives for the work, as these determine the nature of the finances involved and how to manage them.

Where a new portfolio is established or arrangements are being reshaped, the accounting officer and executive board may need to take strategic decisions on how portfolio investment is to be planned and managed before spending starts.

Programmes and projects can start to incur costs as soon as work begins, and these can accelerate quickly. Defining the financial management framework is an early priority so that costs can be budgeted for, met, reported and accounted for from the outset. An initial framework can be put in place and developed as the work expands.

The governance and management framework for finance forms part of the overall governance and management framework for the work and should be integrated with the framework in place for the organisation.

The first step is to assess likely requirements. A short-term project where costs are primarily salary costs held in existing budgets needs a different framework from multi-year work involving different funding streams or external delivery contracts.

This initial view provides a basis for defining the framework. It should cover:

In a portfolio, the framework sets the parameters for managing finance at portfolio level, as well as what is expected of those managing programmes and projects within the portfolio. How this works depends on whether funding is held, managed and allocated through the portfolio, or held and allocated separately.

For organisational portfolios, the framework should be approved by the chief finance officer and accounting officer and the appropriate governance board, usually the organisational portfolio board or investment committee. Below this level, the framework should be approved by the portfolio director.

In a programme or project, the senior responsible owner with support from the appropriate governance board should approve the framework. The framework should set out how the senior responsible owner will exercise financial responsibilities in line with delegated authority, and how any further delegations for day-to-day budget management will work.

Financial planning and control should use existing organisational finance and accounting platforms wherever possible (see 29.6.1.1 on consistency with organisational systems), supplemented by additional processes and specialist tools where needed.

Some organisations provide tools for managing project finances that interface with their existing accounting platforms. For smaller initiatives, spreadsheets are often used for financial data, modelling and analysis. For larger and more complex work, specialised planning and control software, incorporating financial data, can be used.

Financial management in project delivery involves a series of related activities, as shown in Figure 29.1 and considered below. These are iterative and can be applied at portfolio, programme, project and work package levels.

The approach to managing finances should be defined including any processes, methods, tools and techniques to be used. This forms part of the overall governance and management framework for the work (see Chapter 4: Governance and management). The important aspects of this activity are discussed in more detail in 29.6.2.2 on defining the financial management framework. The framework should be maintained to address relevant feedback from its use.

Overseeing includes making sure that:

It is important to monitor the operation of the finance management framework to ensure that it remains effective and appropriate as the work proceeds, particularly if things change.

Finance requirements form a core part of planning (see Chapter 16: Planning) and make up the basis of the financial case within the HM Treasury’s Business case guidance for projects and programmes (requires sign in). The approved financial plan provides a part of the baselined plan against which delivery can be managed and tracked.

The financial plan should be derived from the schedule and determine the level of funding needed through the life cycle. It should provide a summary view for the whole life cycle, and a detailed view for the next phase.

The financial plan should include the:

It should also provide information on:

The financial plan should be set out in financial years on a whole life basis. They should identify different categories of public expenditure, for example resource (administrative or programme), capital and other categories, for example annually managed expenditure (AME). Official Development Assistance (ODA) expenditure should also be identified separately and is subject to a specific governance regime, overseen by the Foreign, Commonwealth and Development Office.

Financial management controls should be implemented as soon possible in the first phase of the work, before any significant spend is committed. Controls can be implemented progressively if needed, but must be reflected in procurement documentation and contracts from that point onwards.

Audit activity often focuses on financial controls around investment and supplier management, and a strong, properly documented and actively-managed control framework is needed to demonstrate proper use of public funding.

Profiling expected spend across the year in line with delivery plans provides a baseline for tracking and managing performance. Profiling should take account of contractual arrangements and when material delivery milestones are expected, triggering the requirements for funding or payments to suppliers.

Actual and committed spend should be recorded in organisational finance and accounting systems as they occur. Spend should be reviewed regularly and forecasts updated, for example as part of the organisation’s monthly financial reporting cycle, covering both annual and multi-year forecasts showing current spending review years and whole life totals.

Actual and forecast spend should be analysed against budget profiles to identify variances. Some variation against profile is usual, but persistent variances can point to delays or other performance issues, leading to underspends, or unforeseen costs or work overruns, leading to unplanned overspends.

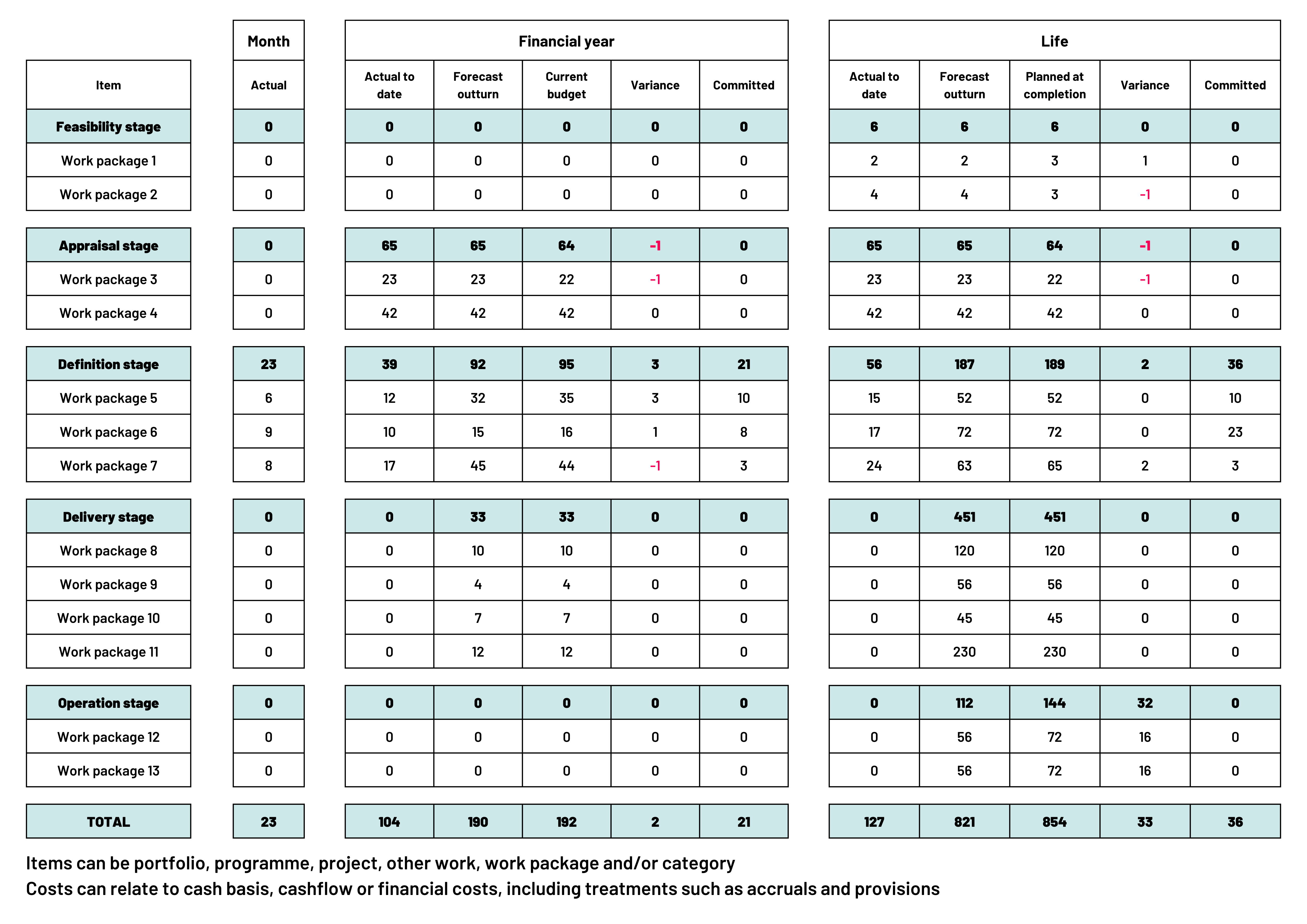

Financial reports and spreadsheets used for tracking should show monthly, annual and whole-life cost profiles, actual and committed spend, and future forecasts, aligned to work breakdown structures. S-curve analysis is a common approach, tracking planned cost, actual cost against schedule or agreed milestones (see Figure 29.2).

Even small variances can point to trends and provide early warning that work going off track. The root causes of variances should be identified and addressed.

Financial status should be reported coinciding with the sponsoring organisation’s reporting cycle but, where systems allow, should be available ‘on demand’ (see Chapter 18: Reporting).

Financial reports should show actual, committed and forecast spend against budget profiles for each expenditure category (admin, programme, capital and others). Reports should provide more detail for the current phase and show a summary view overall. Variances should be highlighted, and where known, the reasons for them explained. Figure 29.3 shows an example of a summary report.

Financial reports can also include other information, for example on funding availability or the effectiveness of financial controls. Financial risks can be flagged here in context but should also be fed into wider risk reporting.

It is important that expenditure is properly recorded and reported on as part of the preparation of annual accounts at organisational level, ensuring that costs incurred or committed are included in the appropriate accounting year.

In a programme or project, following completion of the work, financial reports covering the scope of the work are concluded and financial management arrangements brought to a close. In a portfolio, financial management arrangements normally continue unless the portfolio is fully concluded or substantially reset.

In some programmes or projects, financial data, reporting and accounting arrangements are handed over to operations. This is common where there are ongoing contracts or follow up activities following closure, or where the work moves into a sustainment model with future development carried out as part of business-as-usual operations (see Chapter 36: Transition into use). Where this happens, there should be clear separation between costs within the agreed scope of the work and costs that fall to operations or arise from new development.

Accounting arrangements should be left in place for an agreed period, and at least to the end of the current financial year, so that all spend is accounted for as part of the organisation’s annual accounts and audit and follow up activities can take place.

The effectiveness of financial management should be evaluated as part of closing the work. Financial management information should be archived in accordance with the sponsoring organisation’s information and data retention policies (see Chapter 24: Information and data management). The financial management framework should then be closed.

Updated information about when HM Treasury approvals process applies, added detail on expenditure classifications and a reference to the Consolidated budgeting guidance, updated the fraud impact assessment reference from the Fraud Risk Assessment Core Discipline to the Professional standards and guidance for fraud risk assessment in government, updated the financial case reference from the Five Case Model to the Business case guidance for projects and programmes, updated the accounting officer assessment requirement to include publication of a summary, removed references to the Finance Career Framework, the Aqua Book, the Orange Book and the Project Accounting Principles from the further reading list, and added the Public Sector Fraud Authority’s Government Counter Fraud Profession Standards and Guidance and the Consolidated budgeting guidance.

Page permissions updated for public launch.

First published for closed beta consultation.